AI & Future of Work

9 briefs

Give it a good brief and it returns something brilliant. Give it a vague one and it returns something confidently wrong — at ten times the speed you could have been wrong on your own. Bad framing of a research question returns a convincing analysis of the wrong thing. A weak strategic instinct, run through AI, becomes a polished deck no one questions.

AI drafts the proposal, summarises the meeting, builds the slide deck — and everything looks right. Until you need to use it. The text was there, but the understanding was not. It shows up in a strategy that sounds solid but is impossible to execute, an answer that is right on paper but wrong for the actual moment.

When you ask AI to "clean up the document," it removes the footnotes. When you say "shorten this," it cuts the sections you needed. When you say "make it more professional," it overwrites the tone you spent time building. The gap is between the context in your head and the context the AI has. A precise instruction saves the rest.

The recommendation logic is elegant in theory: someone who purchased X is likely to want more X — until you are the person who just bought a toilet seat and receives toilet seat suggestions for the next three weeks. Three examples of AI optimising for the measurable over the useful: a CRM flagging every email opener as highly engaged, a demand planner reordering whatever sold last quarter, a hiring algorithm filtering by the last company a successful hire came from. Optimising for the measurable is not the same as optimising for the useful.

The brief sounds reasonable: a go-to-market plan that avoids uncertain markets, a product roadmap without tough prioritisation calls, a pricing strategy tested against every objection before it meets a customer. Technically sound. Commercially unambitious. The sixth entry in the Friday AI Digest — on what impossible constraints do to ambitious work.

AI validates your decisions, mirrors your emotions, and adjusts its tone the moment you seem uncomfortable. The problem is not that AI is empathetic — it is that it is infinitely patient in a way no human ever will be. The capacity to sit with tension, repair relationships after conflict, and collaborate with people who disagree are not soft skills. They are the foundation of functional teams.

When the humans leave, the benchmark leaves with them. AI errors don't announce themselves — they surface as normal output until someone with enough experience recognises something is off. Remove that person and the glitch becomes the new standard, silently compounding until the cost becomes visible.

A Claude-based autonomous agent at PocketOS deleted an entire production database and wiped its backups within nine seconds while attempting to resolve a routine task. Railway restored the database after two days. The second entry in the Friday AI Digest — on what happens when autonomous AI operates without safety guardrails.

Then the AI confidently quotes a statistic that does not exist, recommends a strategy based on a fact that is wrong, and only apologises after the damage is done. The first entry in the Friday AI Digest series — observations on working with Claude Code, ChatGPT and the rest.

Billionaires Insights

1 brief

Customer Experience

1 brief

Brands

4 briefs

In February 2018, Remo Ruffini replaced Moncler's two seasonal collections with 8 simultaneous creative directors — each releasing their own drop, at their own moment, to their own audience. Each collaborator brings a distinct audience: A$AP Rocky's, Rick Owens', Willow Smith's, Jil Sander's — none of which fully overlap. Genius eliminates creative succession risk: Moncler's identity is the model itself, not any individual's vision.

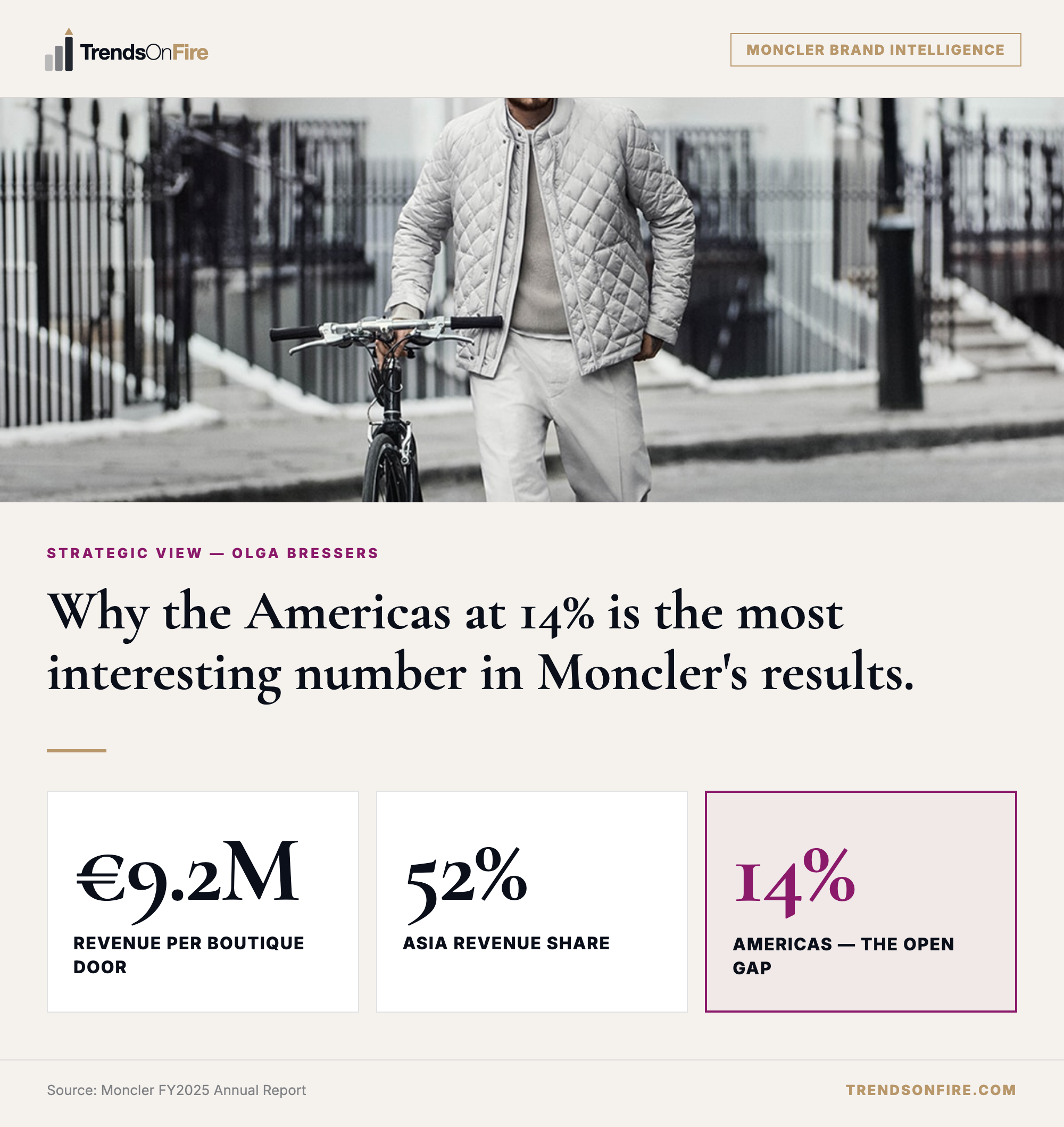

Moncler earns €9.2M per boutique door across 295 locations. Asia-Pacific, Japan and Korea account for 52% of revenues (+7% at constant currency FY2025). EMEA declined 3% — the home market is contracting. The Americas sit at 14% of revenues (+5%) — underdeveloped, earlier in the luxury adoption cycle. That window does not stay open indefinitely. Source: Moncler FY2025 results.

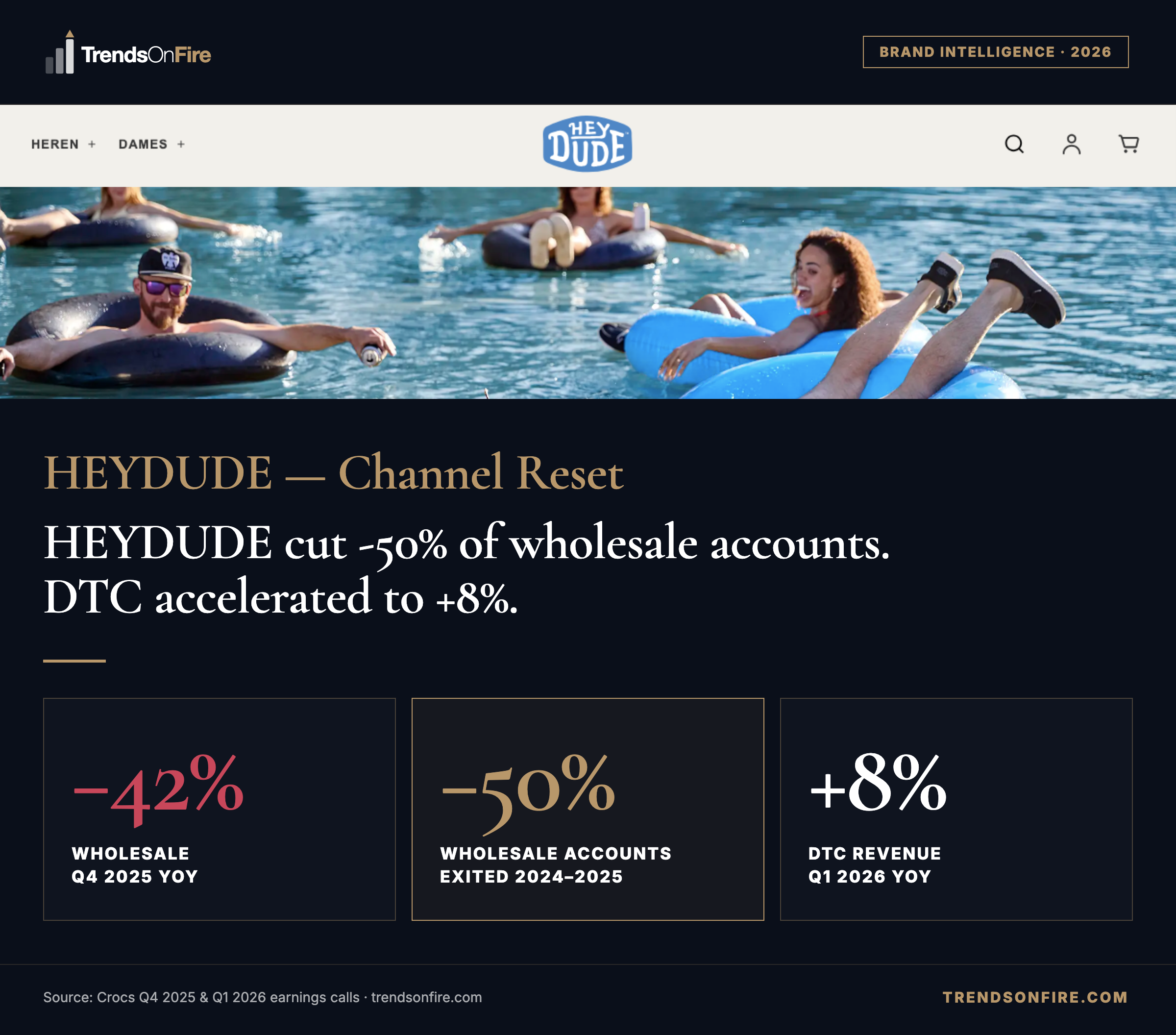

Dick's Sporting Goods and Kohl's are among the accounts that stayed — more than half of the total base did not. Wholesale revenue fell 42% year-on-year in Q4 2025. DTC grew 8% year-on-year in Q1 2026. Brand awareness rose 9 percentage points in 2025, the same year total revenue fell 14%. Gross margin held at 44.8%. CEO Andrew Rees guided for H2 2026 revenue return; Q1 2026 beat consensus. Source: Crocs Q4 2025 & Q1 2026 earnings calls.

The Miele and Zinkann families have held the same 51.1%/48.9% ownership split since 1899. €5.16B in Business Year 2025, up 2.3% on 2024. 19 production plants, 49 subsidiaries, ~100 countries, ~23,000 employees. The AI Product Adviser generates 9% of online sales at 2× the conversion rate of standard browsing. EcoVadis Gold at 84/100 — top 2% globally.

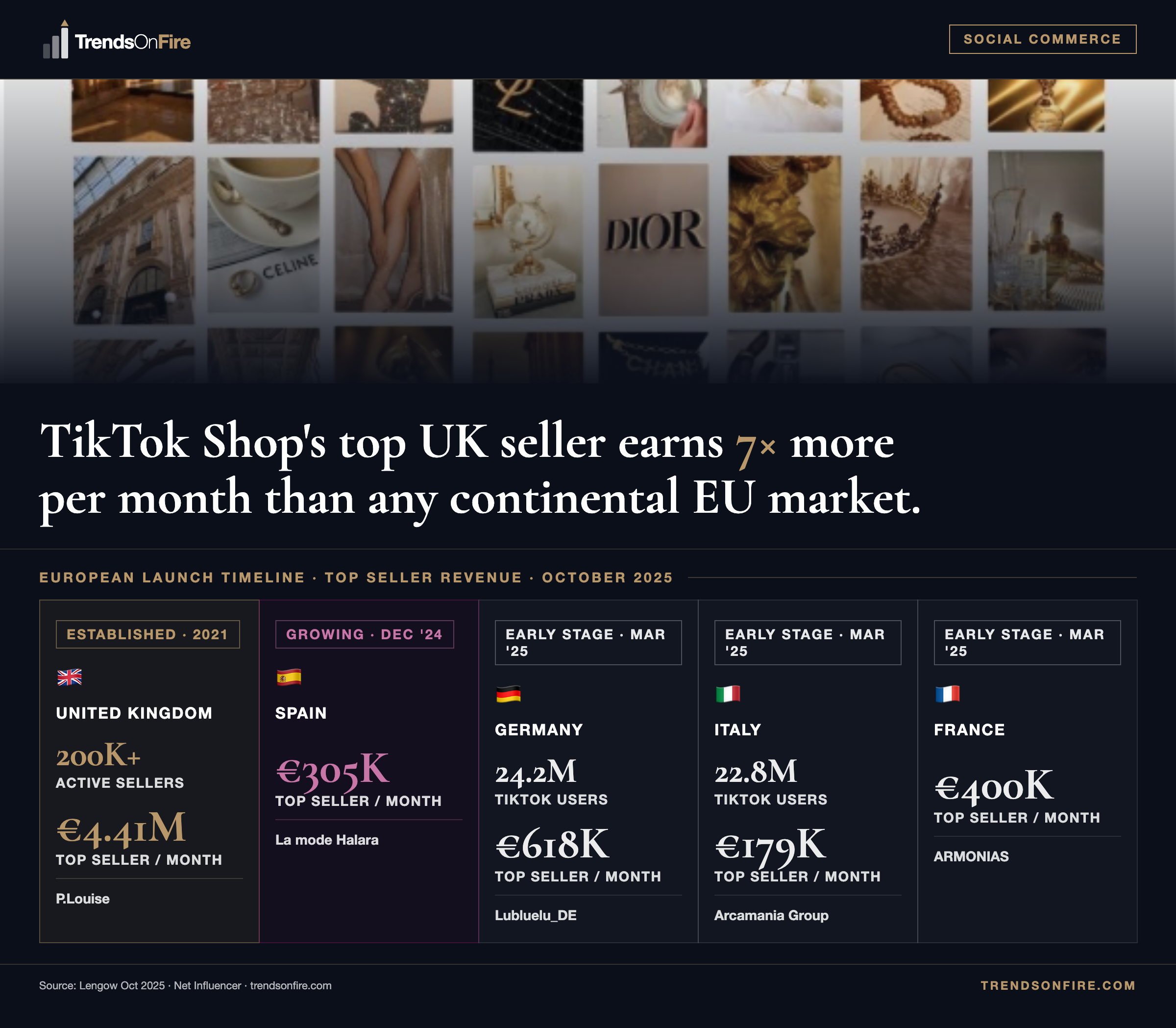

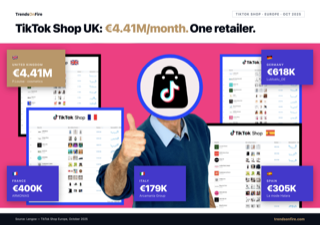

P.Louise earns €4.41M a month on TikTok Shop UK — launched in 2021. Spain, Germany, Italy and France followed in late 2024 and early 2025. Germany's leading seller (€618K) earns what P.Louise made in the UK four years ago. Category leaders in continental Europe have not yet been established. October 2025 figures from Lengow.

Native checkouts are disappearing — Meta exited in 2025, Pinterest never had one, YouTube shows no intention. TikTok Shop stands alone in the West. Now Google Shopping, Walmart+, and legacy brands are building shopping experiences outside the social feed. The social commerce layer is contracting. The commerce layer is moving to owned channels.

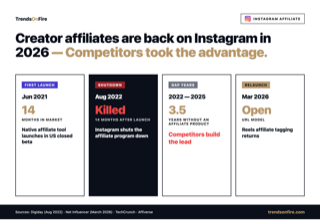

Meta discontinued Instagram's affiliate program in August 2022. During the gap, TikTok Shop generated $5.1B in US GMV with creator commissions and YouTube Shopping enrolled 500,000+ creators with 5x YoY GMV growth. The March 2026 relaunch allows creators to tag any affiliate URL directly in Reels. The question is whether creators who built affiliate businesses elsewhere will return.

P.Louise (UK cosmetics) is generating €4.41M monthly revenue on TikTok Shop. Germany at €618K/month, France €400K/month, Spain €305K/month, Italy €179K/month. October 2025 figures — social commerce revenue is finally materialising at scale across European markets.

TikTok Shop: $15.1B US GMV in 2025, 68% YoY growth, projected 24.1% of US social commerce by 2027. Meta phased out native checkout by September 2025 after six years. Pinterest has 553M monthly users but has not had native checkout since 2018. YouTube Shopping is growing at 5x YoY GMV but does not publish figures.

TikTok Marketing Science/AYTM study (May 2025), 3,000+ luxury consumers across the UK, US, France and Italy. 38% discover luxury through user-generated content, 32% through creator videos, 15% bought a luxury item directly after seeing it on TikTok. The purchasing power is there — the conversion infrastructure is not.

Eleven years of social commerce, from Pinterest's Buyable Pins in 2015 to Meta deprecating Facebook and Instagram checkout in 2025. Six platforms tried in-app checkout. Only TikTok Shop stayed — running the closed loop in Western markets by 2026 while everyone else switched to redirect-only.

Luxury Marketplaces

5 briefs

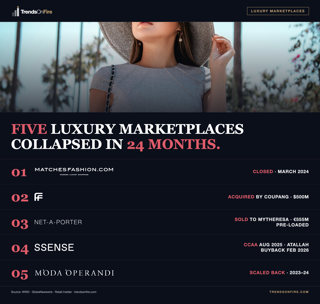

TheRealReal, Vestiaire Collective, Kering, Farfetch — the luxury resale market data. Part of the Luxury Marketplaces report.

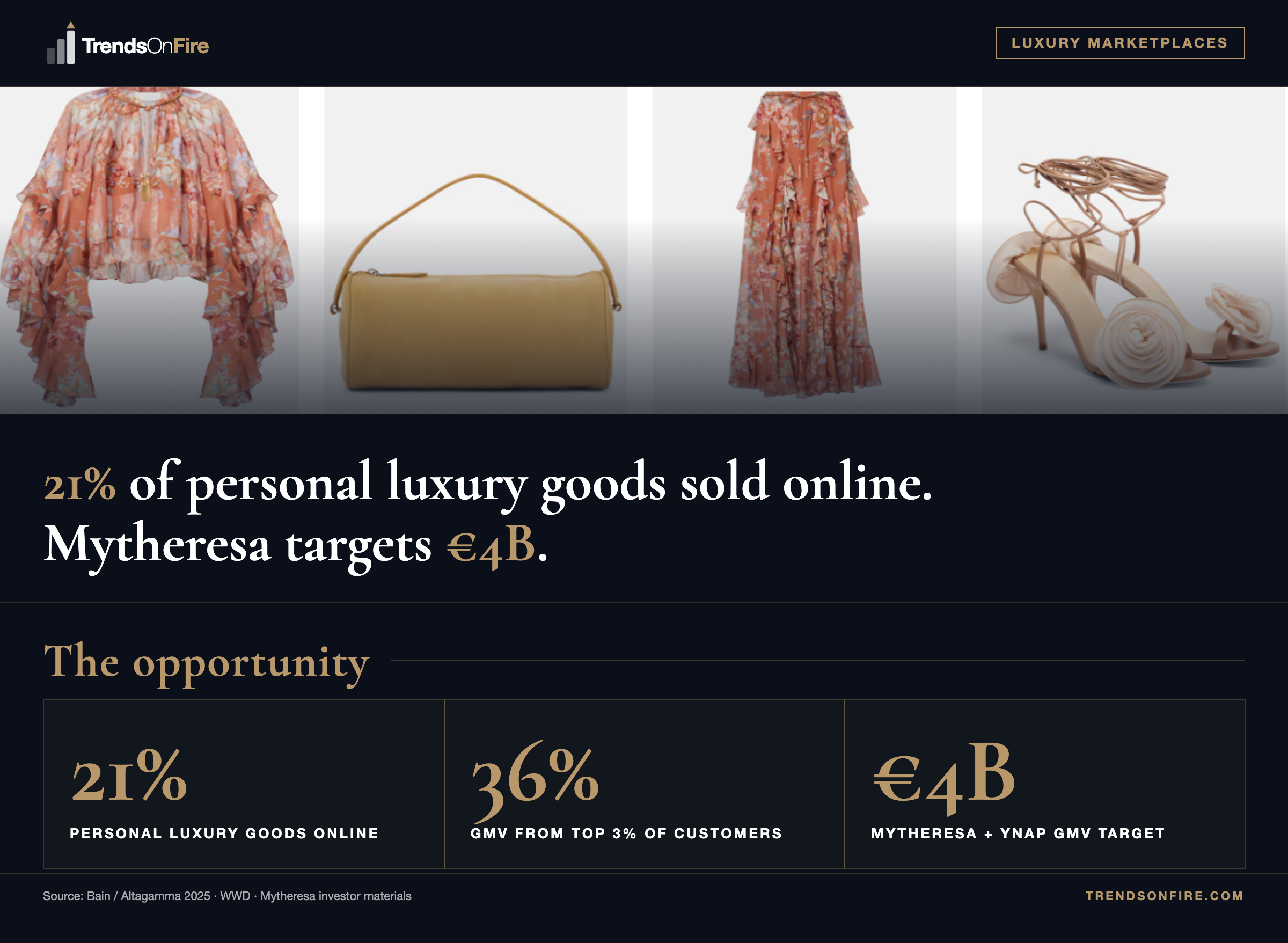

The platforms that failed were built on inventory — buying stock, warehousing it, discounting when it did not sell. Mytheresa ran the opposite: asset-light, curated at fewer SKUs, with 36% of GMV from the top 3% of customers. After Richemont recorded a €3.4B non-cash charge, it transferred YNAP with €555M in net cash. Mytheresa absorbed Net-a-Porter, Mr Porter, Yoox and The Outnet and now targets €4B in combined net sales. Source: Bain / Altagamma 2025.

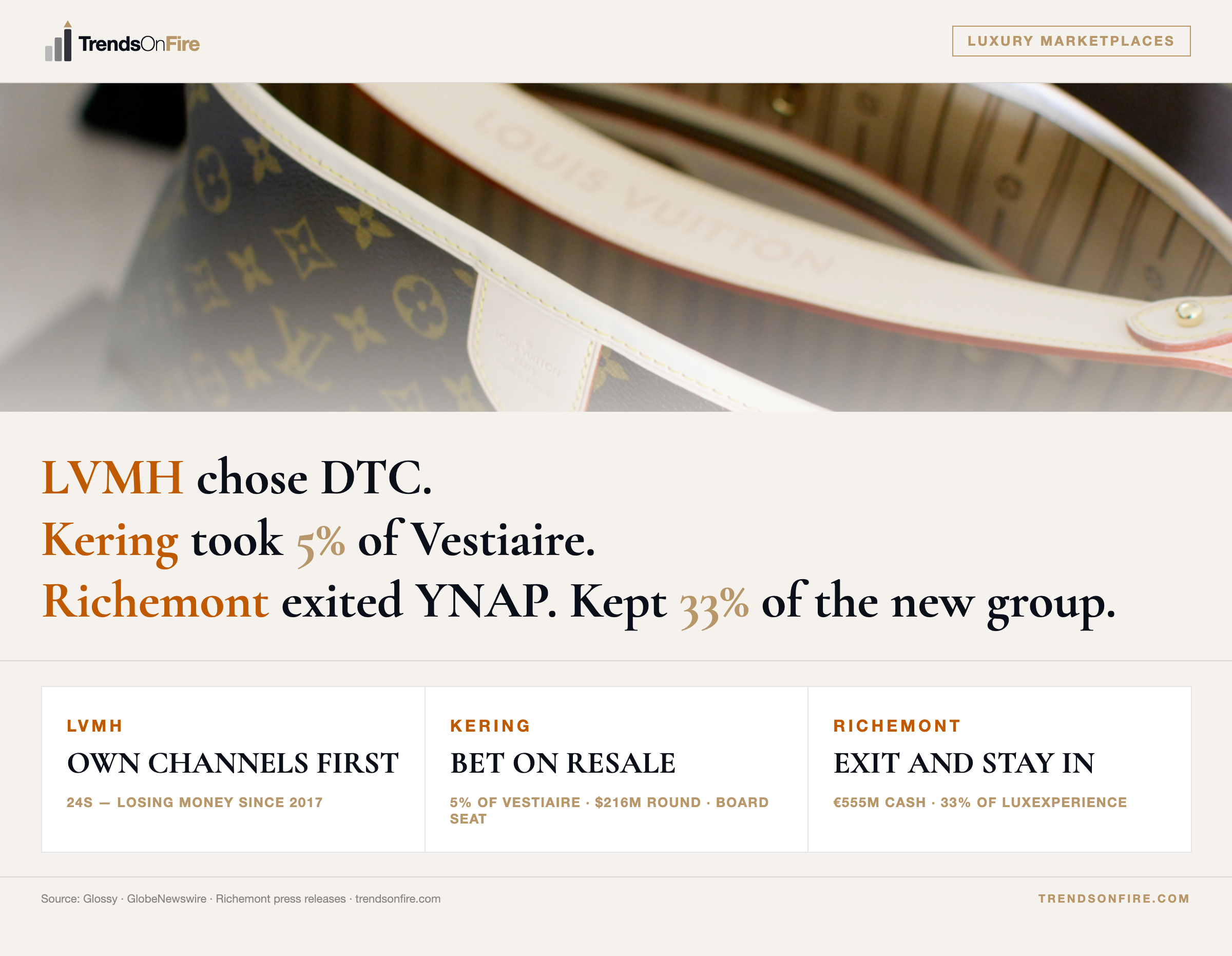

Three conglomerates, three distinct bets on luxury e-commerce. LVMH built 24S as a direct-to-consumer platform in 2017 — Arnault acknowledged it had lost money since launch. Kering acquired 5% of Vestiaire Collective in a $216M funding round, gaining board representation without full platform ownership. Richemont transferred YNAP to Mytheresa in April 2025 with €555M net cash, taking 33% equity in the resulting LuxExperience group — after recording a €3.4B non-cash charge in FY2023.

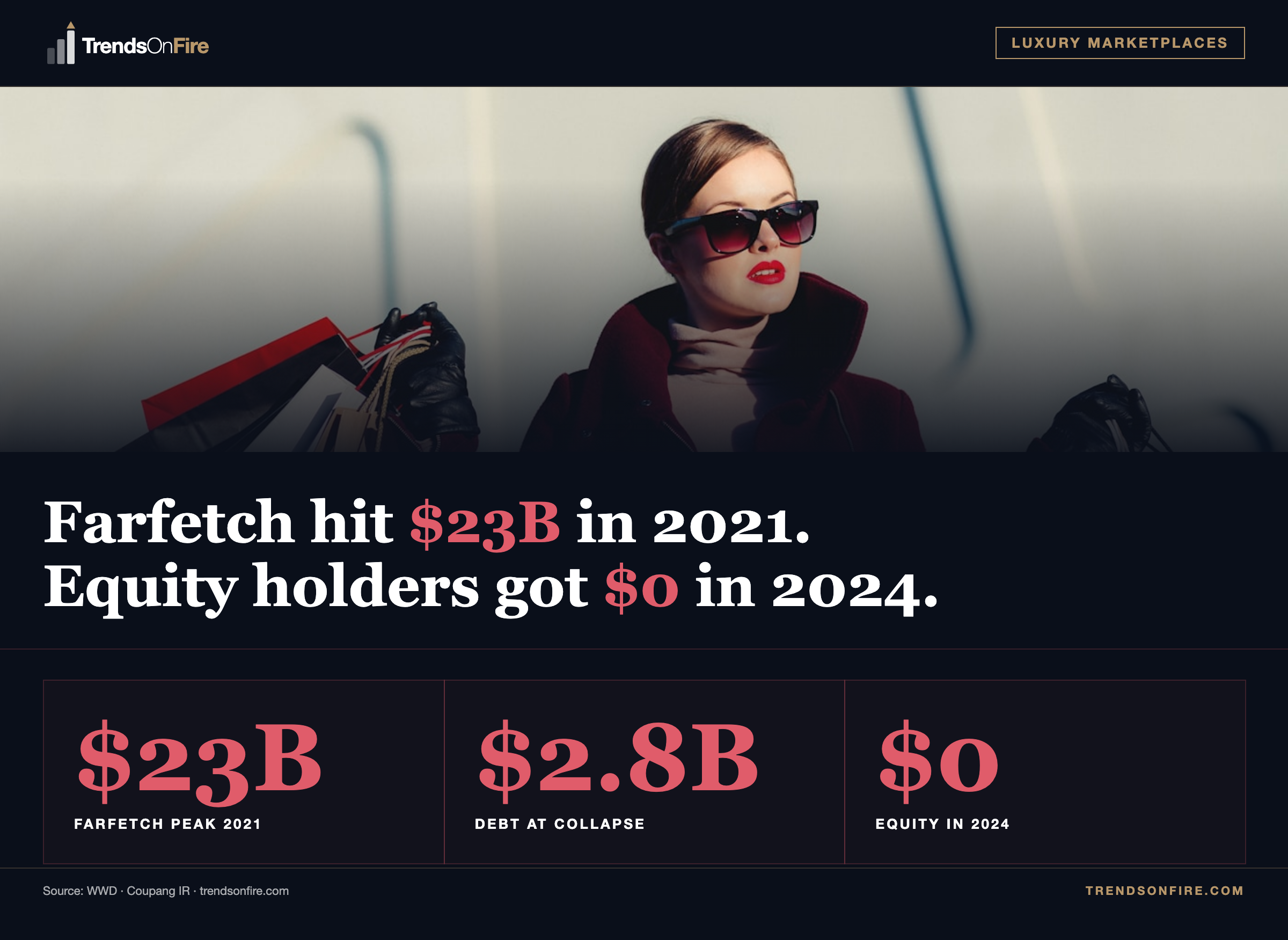

Farfetch went public in 2018 and spent $675M acquiring New Guards Group in 2019, shifting from marketplace to brand ownership with inventory risk. When growth stalled, $2.8B in accumulated debt triggered a crisis by December 2023. Trading was suspended on the NYSE, Fitch downgraded to CC, and Coupang provided $500M emergency financing. The company entered UK pre-pack administration. Equity holders recovered nothing. Under Coupang, Farfetch divested the acquired brands and refocused on its original luxury marketplace purpose.

Farfetch, MatchesFashion, SSENSE, and YNAP (Net-a-Porter) — four platforms collapsed between 2023 and 2024. Farfetch raised $2.6B+ and sold to Coupang for $500M. MatchesFashion liquidated in March 2024. YNAP transferred to Mytheresa in September 2024. Mytheresa is now absorbing YNAP and targeting €4B in revenue by 2030. What the collapse reveals about the luxury e-commerce model.

Tech Recruitment 2026

3 briefs

The Dutch ICT market peaked in mid-2022 at 40,000 open vacancies. Since 2023, supply and demand have been converging. The emergency conditions are over. Today's anomaly: AI Engineer is the #1 growing role in NL tech — every other specialism is flat or down. The real question is whether the recovery looks like 2022, or like a fundamentally different, smaller market structured around AI.

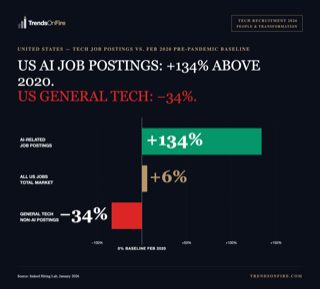

Dice Tech Job Report and Indeed Hiring Lab data show a market split: AI-related postings are 134% above pre-pandemic levels while generalist tech sits 34% below. AI fluency is no longer a differentiator — it has become baseline in 71% of US tech job postings. The divergence spans every market: US, Europe, Netherlands.

IBM surveyed 2,000 CEOs with median revenue $5.8B. Three key findings: 76% are hiring a Chief AI Officer, 61-point gap between skills available and daily AI use, 57% of CAIOs promoted internally. The supply-side constraint is not access to AI expertise — it is integrating AI across an entire organisation.

Brand Discovery

1 brief

Fashion Technology

2 briefs

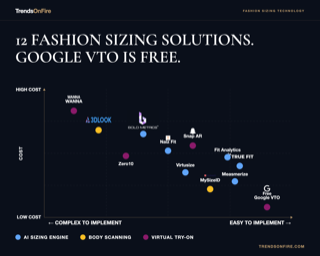

The 12 solutions span AI sizing engines, body scanning tools, and virtual try-on platforms. Google VTO launched May 2025 free for Google Shopping brands, with Macy's, Kohl's, Walmart and Nordstrom live at launch. Key platforms: True Fit (80M+ profiled shoppers), Bold Metrics (AI body model from 2 questions), Naiz Fit (published 14% returns reduction), Fit Analytics (4B monthly recommendations), WANNA (luxury AR, enterprise pricing), Snap AR, Virtusize, Measmerize, MySizeID, 3DLOOK, Zero10.

Seven years of sizing technology: ASOS Fit Assistant used purchase history in 2018, Nike Fit scanned feet with 13 AR data points in 2019, Zalando's two-photo body scan cut returns by 10% in 2023, Zara launched a 3D avatar from a single selfie across 6 markets in December 2024, Amazon opened a generative AI try-on API via Bedrock in July 2025. Google entered with free try-on for Google Shopping brands in May 2025.

Humanitarian Logistics

5 briefs

Acute food crises expanded from 258 million to 295 million people between 2022 and 2024 — while WFP's reach contracted by 22%. The 2025 data covers only 47 of 65 countries, meaning the actual scale is likely understated. The gap between capacity and need is widening.

A $7.6 billion drop in three years. Consequences: 6,000 staff positions eliminated, scaled-back operations in active crisis zones, and no reserve mechanism to buffer funding gaps. The 2025 figure came mid-year — the final total may be lower still.

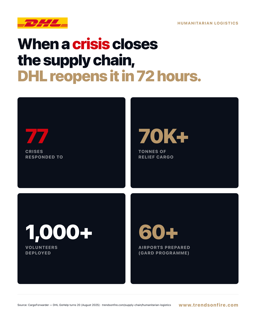

When a crisis hits, the local supply chain collapses — airports stop functioning, cargo piles up, aid cannot move. DHL GoHelp has spent 20 years training 1,000+ volunteers to restore cargo operations in crisis zones within 72 hours, across 60+ airports in 30 countries.

WFP eliminated 7,000 positions (30% of workforce). UNHCR cut 5,900 (30%). IOM reduced headcount by 6,000 (35%). The cuts represent a contraction in the world's most complex logistics networks, driven by funding shortfalls after the US reduced its share of WFP's budget from 46%.

WFP feeds 124 million people. UNICEF procures $5.6 billion in supplies. UNHCR runs a $10 billion programme. All of it is run from Europe. The world's humanitarian operations are designed, procured and dispatched from 8 European cities — Rome, Copenhagen, Geneva, Brindisi, Bordeaux, Bonn, Oxford, Budapest.

Circular Economy

3 briefs

H&M FY2025: 91% recycled or sustainably sourced materials (up from 89%), resale at 0.8% of group turnover (up from 0.6%). Resale grew 27% year-on-year to SEK 1.8B — but it remains a fraction of total revenue. Material sourcing goals are largely achieved. The circular infrastructure is still at the beginning.

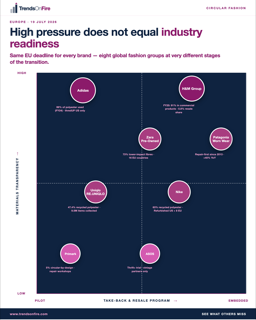

Eight global fashion groups face the ESPR unsold stock ban from 19 July 2026. A readiness matrix shows where each brand stands on materials and take-back programmes.

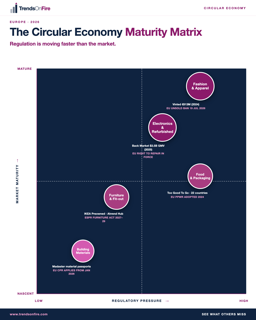

Between July 2024 and mid-2028, five consumer categories in Europe shift from voluntary sustainability to mandatory compliance under ESPR.

Brand Collaborations

2 briefs

Swatch × Audemars Piguet, H&M × Stella McCartney, Gap × Victoria Beckham, Supreme × MM6 Maison Margiela — four collaborations, one formula: luxury signature, mass price point, controlled scarcity. The H&M × Stella McCartney Falabella clutch sold for €49, versus €491 for the original. Dublin sold out in 2 hours; by noon it was reselling at 3× on Vinted. The collaboration is not a product launch. It is a price-access deal — luxury distributed at mass scale, with scarcity doing the marketing.

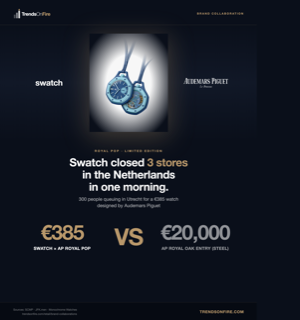

The Swatch × Audemars Piguet Royal Pop launched on 16 May at selected boutiques worldwide. In Amsterdam, Leidschendam, and Utrecht, crowds grew unmanageable before 10:00 and three stores cancelled the launch. MoonSwatch precedent: a €260 Omega collaboration boosted original Speedmaster sales by 50%. The Royal Pop sells the DNA of a €20,000 watch at €385 — a 98% discount on brand equity, not the product.

Electric Vehicles

3 briefs

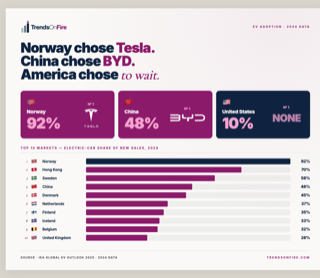

Tesla Model Y is the top-selling vehicle overall in Norway. BYD outsells every Western competitor inside China. The US has fragmented state incentives and no dominant domestic player. Europe occupies the middle band, with VW, BMW and Volvo gaining ground against Tesla and BYD. Source: IEA Global EV Outlook 2025.

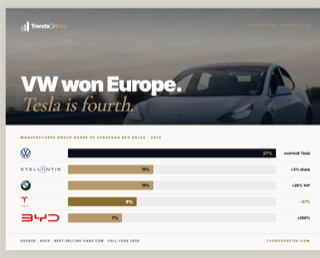

VW Group leads Europe's battery-electric market in 2025 with 27% share, with the VW brand growing BEV sales 56%. Tesla dropped to 9% on a 26.9% YoY decline (from 326,525 to 238,656 units). BYD surged 268.6% to 7%. Stellantis and BMW Group both gained share and now sit ahead of Tesla.

The Netherlands approved Tesla Full Self-Driving (Supervised) on 10 April 2026. But Level 2 means you are still the driver. SAE autonomy levels explained.

Education & Government

2 briefs

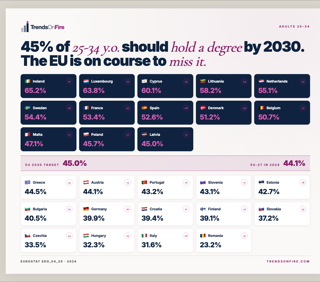

EU average tertiary attainment for 25–34 year-olds: 44.1% in 2025, against the 45% target for 2030. Ireland leads the EU at 65.2%, Luxembourg at 63.8%, Lithuania at 58.2%. Germany sits at 39.9% with its vocational tradition. Italy at 31.6% and Romania at 23.2% mark the central EU-27 gap. 13 member states are above target, 14 below.

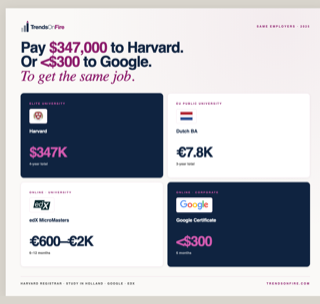

EU public university tuition averages €7,800. An edX MicroMasters costs €600–€2,000. Deloitte, Verizon, Target and others now formally recognise Google certificates. By 2030, what will employers actually value: signal or skills?

Supply Chain

3 briefs

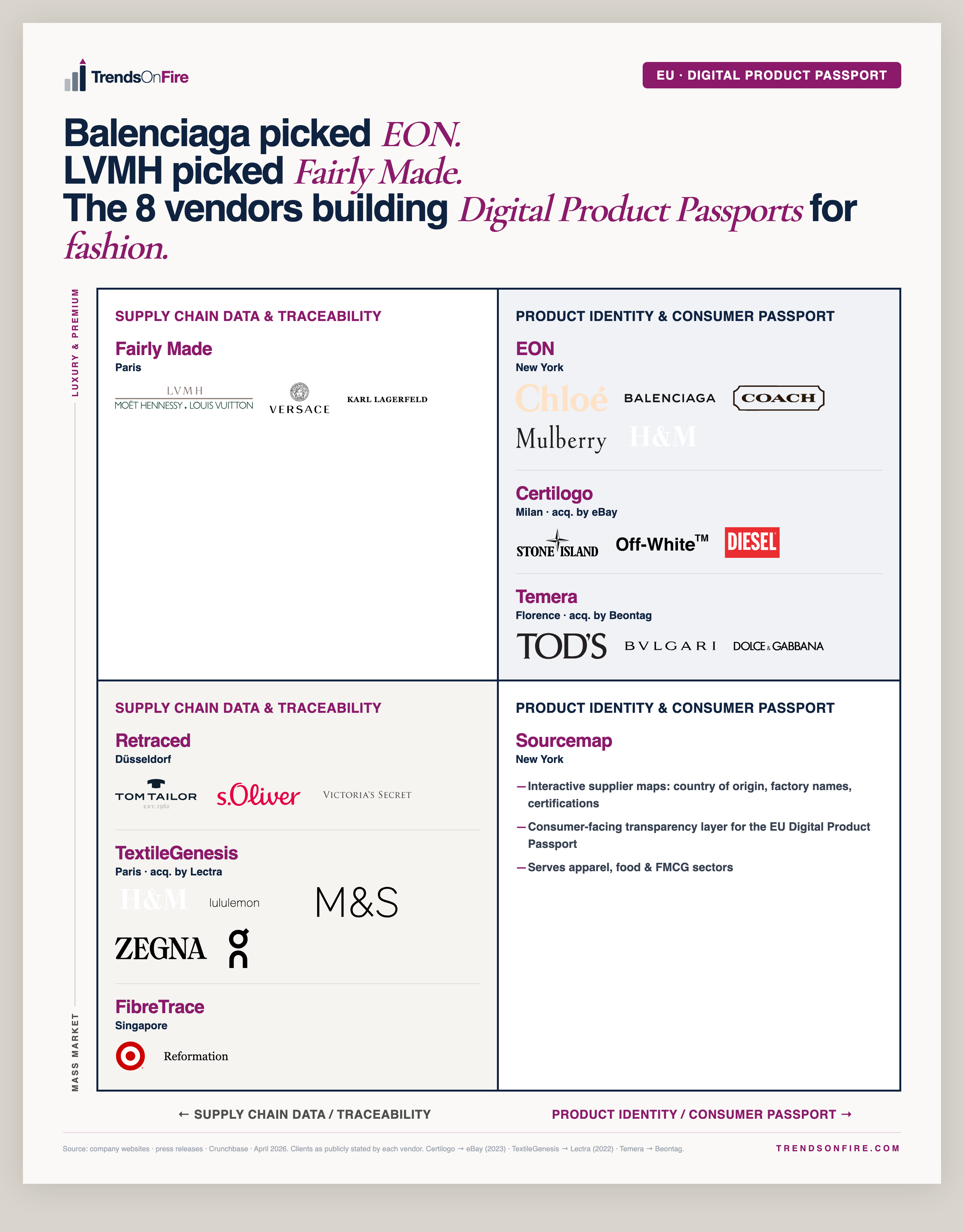

The DPP vendor landscape splits by two dimensions: supply chain traceability vs product identity, and luxury vs mass market. Eight vendors mapped across four quadrants — with the brands that selected each one.

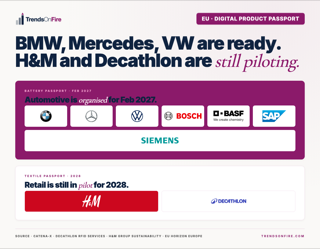

The Catena-X consortium — BMW, Mercedes-Benz, VW, Bosch, BASF, SAP, Siemens — is building the shared data architecture for the EU battery passport, mandatory from 18 February 2027. H&M piloted on Men's Essentials in 2022. Decathlon has 100% RAIN RFID coverage since 2019. Most apparel brands are still waiting for the 2028 delegated act.

The EU Digital Product Passport rolls out in waves across six years. Batteries go first — automotive is organised around Catena-X. Fashion retail, heavy industry, furniture and tyres follow. The full compliance timeline by product category.

Social Commerce

7 briefs